Investors swarmed all over SpaceX’s historic IPO and are hyped about public debuts for OpenAI and Anthropic later this year, but they’re also wondering if the good times will keep rolling.

While the stock market has demonstrated stunning durability amid shocks like President Donald Trump’s trade war and Iran war, the flood of new shares has Wall Street debating if a downturn is due soon.

In addition to the $75 billion SpaceX raised, its AI rivals are expected to tap investors for tens of billions more. And that’s after Google parent Alphabet netted $85 billion from a secondary stock offering earlier this month.

“While the mood music is relatively positive at the time of writing, history suggests caution is in order: major IPOs and periods of high issuance of equity have often preceded peaks in the US equity market,” Jonas Goltermann, chief markets economist at Capital Economics, said in a note on Friday.

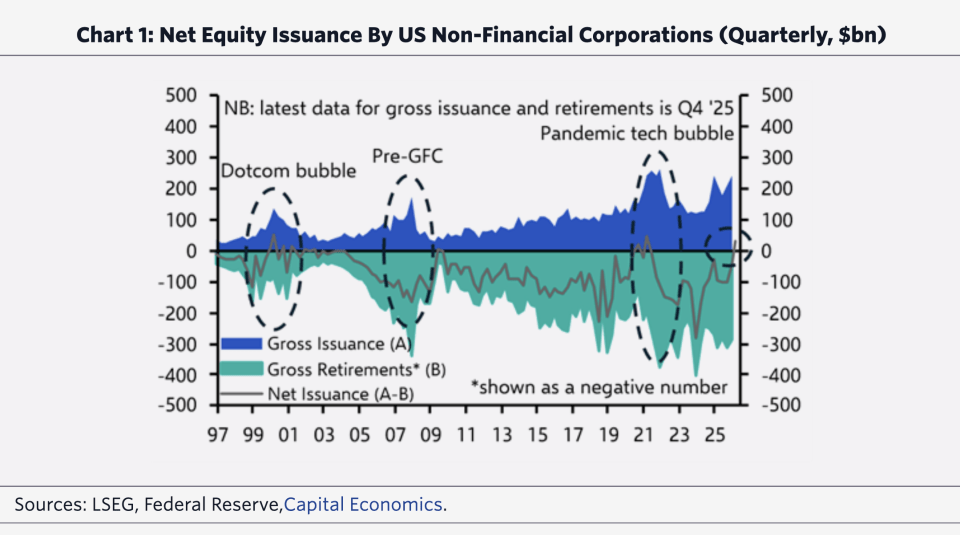

He pointed out that gross equity issuance in the U.S. surged in 1999, 2007, and 2021—years that were all followed by bear markets—with recessions also coming after the tech bubble and housing bubble.

In fact, even before SpaceX’s IPO and Alphabet’s offering, net equity issuance by U.S. non-financial companies had already turned positive by the first quarter of this year, Goltermann added.

And with IPOs for Anthropic and OpenAI on deck, he said it’s reasonable to assume issuance for this year will resemble what came in 1999, 2007 and 2021.

To be sure, the current market rally has been driven by strong earnings and not pure speculation, while valuations don’t look so overextended when compared to other peak eras, Goltermann noted.

“That said, there are more and more similarities between the current market environment and that around previous equity market peaks, which suggests that the AI equity boom may be approaching its final innings,” he warned.

But analysts at Deutsche Bank drew a much more bullish conclusion while crunching the numbers in a different way.

They singled out upcycles in new share supply and looked at the median volume of issuance compared to the S&P 500’s performance. The data showed that equity issuance waves typically coincided with strong stock market returns—not market stress.

“The reason is that companies tend to issue when equity demand is strong, earnings momentum is healthy and investor risk appetite is elevated,” analyst Jim Reid wrote on Tuesday. “In other words, causality usually runs from strong markets to issuance, rather than issuance causing markets to fall.”

In fact, issuance waves over the past three decades produced median equity returns of about 8% over three months and more than 20% over 12 months, according to Deutsche Bank, with the main exception being the Great Financial Crisis when companies scramble to raise capital via stock offerings.

The current upcycle started well before 2026. U.S. stock issuance has jumped from a quarterly run rate of $30 billion in early 2023 to roughly $120 billion now.

“Crucially, today’s backdrop is characterized by very strong equity demand. Inflows are booming, supported by robust earnings growth, still-modest overall equity positioning and elevated buyback activity,” Reid said. “Household balance sheets also retain significant capacity to absorb new supply. As with prior IPO waves, strong demand — not excess supply — is likely to be the defining feature.”

This story was originally featured on Fortune.com