President Donald Trump’s decision to bomb Iran is rattling global oil markets, threatening to reignite inflation—and according to Morgan Stanley’s Global Investment Office, it could cost Republicans their Senate majority and send the national debt into overdrive.

The firm’s investment strategist and head of U.S. policy, Monica Guerra, published a detailed analysis Thursday warning about the obvious: The incumbent’s party tends to lose seats in midterm elections, and this particular conflict has triggered one of the most consequential energy-supply shocks in recent memory. The implications stretch from the Federal Reserve’s interest rate path all the way to November’s midterm ballot box.

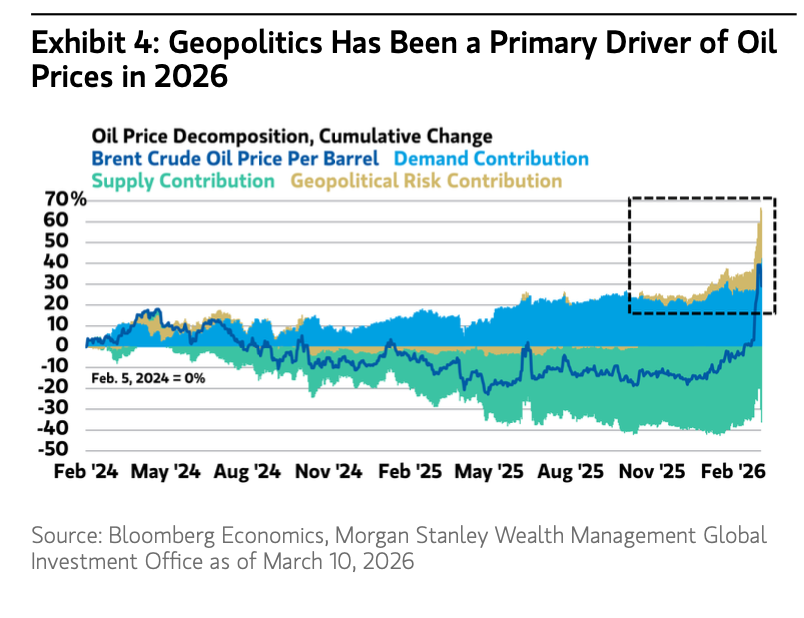

The Strait of Hormuz is closed—and oil just hit $100

On Feb. 28, U.S. and Israeli forces launched coordinated missile strikes on Iran’s nuclear facilities, military infrastructure, and senior leadership. Iran retaliated against Israel, U.S. bases, and regional allies—and the Strait of Hormuz, through which roughly 20% of global oil supply flows, or approximately 21 million barrels per day, effectively shut down.

Crude prices surged above $100 a barrel almost immediately. Oil is now up over 51% for the year to date. The 10-year U.S. Treasury yield has jumped 27 basis points since the conflict began, reflecting renewed inflation fears and growing concern about deficit spending.

This is now an inflation problem—and a Fed problem

Guerra’s team warned oil shocks of this magnitude have historically delivered a 70-basis-point boost to headline CPI within three months. Core inflation, by contrast, would see only a modest impact—but that calculus changes fast if elevated prices persist.

“If higher oil prices persist,” the report warned, “the Fed’s reaction function could be complicated, supporting a higher fed funds rate for longer.” That’s bad news for an economy already navigating tariff pressures and a ballooning deficit.

Why Republicans should be worried about the Senate

Here’s the political math Morgan Stanley lays out: Since 1922, the sitting president’s party has lost an average of 30 House seats and four Senate seats in midterm elections. Republicans currently hold a 53–47 Senate majority—a margin Morgan Stanley says could narrow significantly with a prolonged energy shock.

The firm’s base case is that the GOP loses the House and keeps the Senate. But a sustained oil shock could tighten the Senate race in ways that scramble that forecast.

The reason is simple and visceral: gas prices. The bottom 20% of consumers spend four times more of their budget on energy than the top 20%. Rising prices at the pump, Morgan Stanley notes, are “one of the most visible signs of daily affordability for most voters”—and affordability is the top voter concern heading into the midterms.

On a related note, UBS chief economist Paul Donovan warned on Thursday not to underestimate one key indicator of inflation: the price of a Snickers candy bar.

“The lived reality is somewhat different from the headlines,” he wrote on Thursday. It’s true that owners’ equivalent rent helped lower inflation, but he called that “a fantasy price no one pays.” Used car prices fell, too, but people don’t buy a used car every month.

“Grocery price inflation has accelerated recently, with big increases for beef, coffee, and chocolate,” he wrote. “A Snickers bar’s price is important in shaping inflation perceptions.”

The war could turbocharge the debt

Guerra also noted the fiscal dimension in voters’ concerns. The conflict has injected fresh momentum into Trump’s $1.5 trillion defense spending request for fiscal year 2027—a proposal that would push military outlays to 4.6% of GDP, the largest annual increase in at least 60 years. The U.S. reportedly spent $5.6 billion on munitions in just the opening 48 hours of the war, accelerating bipartisan pressure for $50 billion in supplemental defense spending.

Morgan Stanley warns that elevated war-driven government spending will “modestly weigh on debt and deficits” and push up U.S. Treasury term premiums—the additional yield investors demand to hold longer-term government bonds. In plain terms: Borrowing gets more expensive just as Washington needs to borrow more.

Markets are holding—for now

Despite the turbulence, U.S. equities have remained largely flat since the conflict began, buoyed by strong energy sector performance and a global rotation into dollar-denominated assets. International stocks, as measured by the MSCI World ex-U.S. Index, are down 6%—reflecting Europe and Asia’s greater exposure to the energy shock.

History offers some comfort: The S&P 500 has gained an average of 8.4% in the 12 months following major geopolitical risk events over the past 75 years. But Morgan Stanley was explicit that duration is the key variable. The longer the Strait stays closed and the bombs keep falling, the harder those historical averages are to count on.

For this story, Fortune journalists used generative AI as a research tool. An editor verified the accuracy of the information before publishing.

This story was originally featured on Fortune.com